Taxed Twice: The RSU Mistake That's Probably on Your Last Tax Return

There's a real chance you overpaid your taxes on your RSUs last year — and your return looks completely correct. The 1099-B your whole return is built on reports a $0 cost basis by design, quietly taxing you twice on the same income. Here's how the trap works, how to fix it on Form 8949, and how to claw back what you overpaid within the three-year window.

The Estate Plan You Rushed in 2025 — and What to Do With It Now

For three years the advice was "use it or lose it," so you funded the trust and made the gifts before the December 31 deadline. Then the deadline disappeared — the exemption didn't fall to $7 million, it climbed to $15 million and became permanent. Here's what still works, what solved a problem you no longer have, and the six things worth re-checking now.

The ISO Trap Just Got Sharper: How the 2026 AMT Change Can Tax Money You Never Received

You exercised your incentive stock options and didn't sell a share—then came a five-figure tax bill on a gain you can't spend. That's the AMT, and in 2026 the trap closes faster than ever. Here's how it works, in plain English, and the moves that keep it from catching you.

Money Advice That Sounds Smart and Quietly Makes You Poorer

Some of the worst money decisions don't feel like mistakes — they feel responsible. Here are the money clichés that sound the smartest and quietly cost high earners the most, and the rules-over-feelings reframes to use instead.

The QSBS Overhaul: The Founder Tax Break That Just Got a Major Upgrade — and the Trap Hiding Inside It

On July 4, 2025, the rules for tax-free founder exits quietly changed. QSBS got its biggest upgrade in a decade — but the same law drew a hard line through the calendar, and the founders who don't know which side of it their shares fall on are the ones who'll leave money on the table.

The NQDC Election You Can't Take Back: How Executives Decide How Much to Defer

Every fall, your company hands you a deferred compensation election form with a deadline. Most executives respond one of two ways: they defer aggressively because the tax savings look obvious, or they skip it entirely because the rules feel complicated and the money feels locked away. Both are decisions — and both are usually made for the wrong reasons. This piece breaks down what a nonqualified deferred compensation plan actually is, the two failure modes that cost executives the most, and the framework for deciding how much to defer before you sign a form you can't unwind.

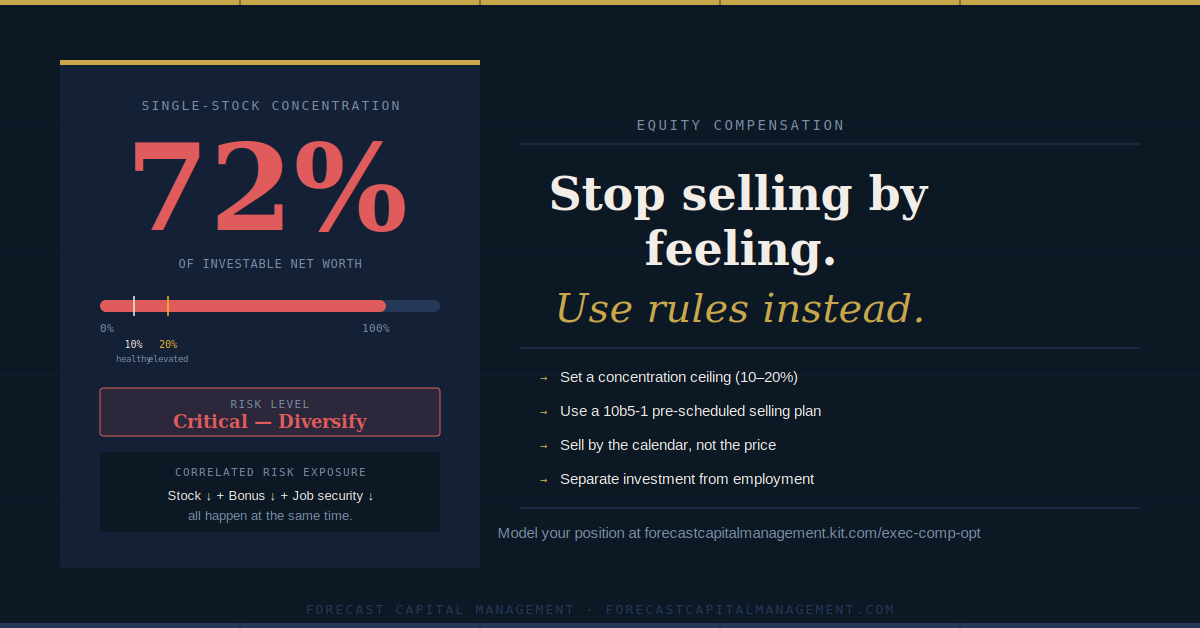

The Executive's Guide to Selling Company Stock Without Regret: Rules Over Feelings

Most executives know they should diversify their company stock. They just never pull the trigger. The problem isn't discipline — it's that selling by feeling is the wrong approach entirely. This piece breaks down the concentration risk most executives don't see, why the tax deferral argument has real limits, and the rules-based selling framework — concentration ceilings, 10b5-1 plans, calendar-based selling — that removes emotion from the equation before your next trading window opens.

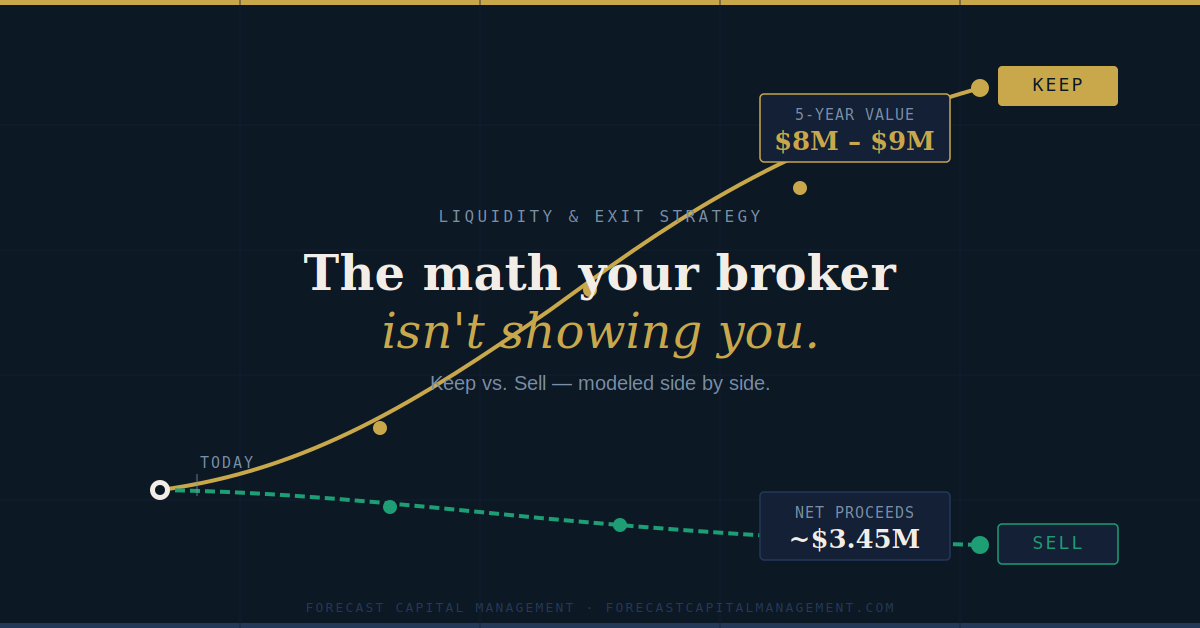

The Keep vs. Sell Decision: The Math Your Business Broker Isn't Showing You

Most exit planning conversations focus on the offer — the multiple, the structure, the headline number. What rarely gets modeled is the other side of the equation: what your business would be worth if you didn't sell. The Keep vs. Sell framework puts both paths side by side, with the real post-tax, post-fee numbers, so you can make a deliberate decision — not a default one.

The NQDC Trap: Why Executives Either Over-Defer or Do Nothing — And Both Cost Them

Most executives either max out their NQDC deferrals without a plan—or ignore the benefit entirely. Both can backfire. This post breaks down the three levers that matter: election timing, the real tax-deferral math (including future bracket stacking), and the counterparty risk you’re taking with your employer. If you’re using NQDC, this is how to make it intentional, sized, and coordinated with the rest of your comp.

The “RSU Withholding Isn’t a Plan” Trap (And How Execs Fix It)

RSU withholding is a default payroll setting—not a strategy. For many high earners, the standard “sell-to-cover” withholding rate doesn’t match their real all-in tax rate once you stack salary, bonus, equity income, and state taxes. That gap is why executives get surprise tax bills even in good years. This post breaks down the “withholding isn’t a plan” trap and gives a simple checklist to pressure-test your RSU and tax strategy.

How Founders and Executives Are Actually Using AI (Without the Hype)

AI isn’t a strategy. It’s a lever.

Used well, it doesn’t replace your judgment—it removes the low-value friction that steals your time: rewriting the same email, rebuilding the same deck, re-explaining the same decision, and re-reading the same long document.

This post is a practical field guide to how founders and executives are actually using AI to create efficiency—across communication, operations, and decision support—without turning their business into a science project.

Oil Shocks Don’t Repeat. They Rhyme: A Short History for Today’s Iran Risk

Oil shocks don't repeat. They rhyme. Not because the headlines are the same, but because the sequence is familiar: a supply shock hits, narratives harden, policymakers respond, and investors treat a temporary disruption like a permanent new world. This essay walks through 1973 and 1979, then maps four scenario lanes for today's risks—without pretending to forecast which one we're in.

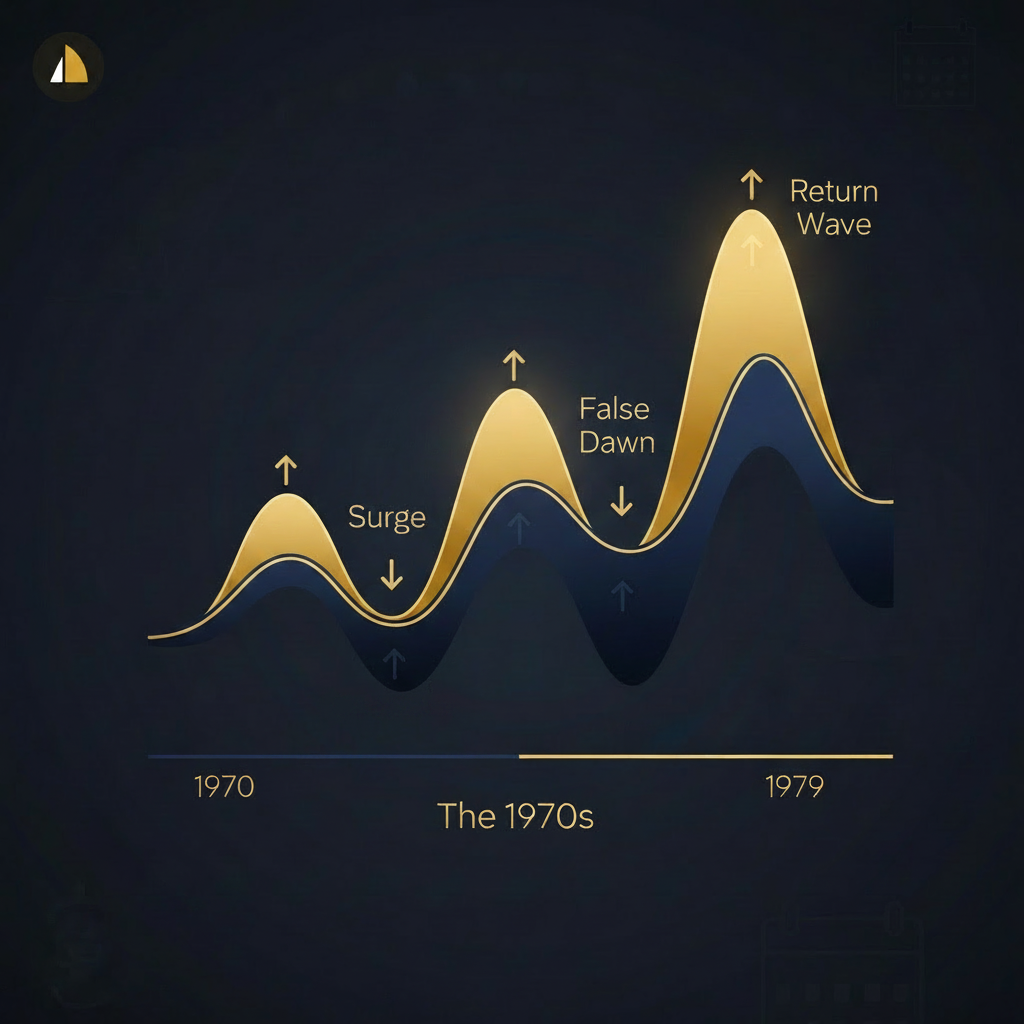

The 1970s Called: Inflation Wasn’t a ‘One-Time Event’ Then Either

Inflation has a funny way of messing with people twice. First, it hits your budget. Then it hits your beliefs.

The 1970s are the reminder most investors skip: inflation didn’t show up as one spike that politely went away. It came in waves—surge, response, cooldown, relief… and then another round. That pattern is what breaks good plans, because it tempts smart people to treat a regime shift like a temporary headline.

This post is a calm, practical playbook for an “inflation comes in waves” world—how to protect cash flow, avoid tax-timing surprises, and write decision rules you can follow when the story changes.

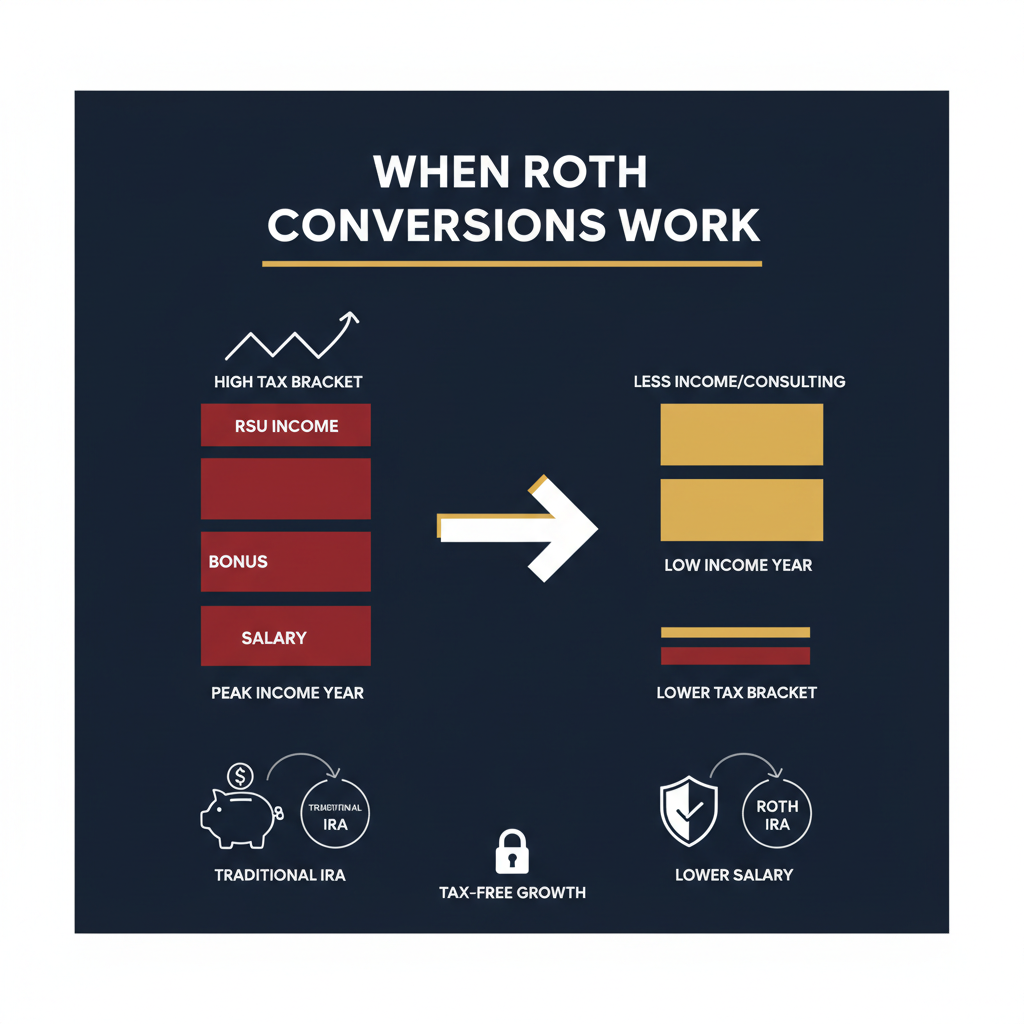

Roth Conversions for High Earners: When They Work (and When They Don’t) — W-2 Executive Edition

If you’re a high-earning W-2 executive, a Roth conversion can be either a smart move—or an expensive one. The strategy is simple: you voluntarily pay ordinary income tax today to move pre-tax retirement dollars into a Roth, aiming for tax-free growth and withdrawals later. The catch is that for many executives, “today” is already a peak tax year once salary, bonus, and RSU income stack together. In other words: a conversion can accidentally pour gasoline on an already-hot bracket.

The better approach is rules-based. Roth conversions tend to work best in opportunistic years—income dips, job transitions, reduced bonus years, or down-RSU years—when you can convert at a lower marginal rate and “fill up” a bracket on purpose. This post lays out a practical checklist to decide whether a conversion makes sense, how to avoid common pitfalls (like paying the tax from the retirement account), and how to think about related strategies like the backdoor Roth and mega backdoor Roth without mixing them up.

The Due Diligence Checklist: 15 Questions Before Any Alternative Investment

Alternative investments can be useful tools—but they can also be expensive distractions. The biggest mistake high earners make isn’t picking the “wrong” fund. It’s buying an alternative for the wrong job (FOMO, a persuasive pitch, a tax headline) without understanding the real tradeoffs: liquidity, valuation, leverage, fees, and how the investment behaves when markets get stressed.

This checklist gives you 15 questions to ask before any alternative investment—private equity, private credit, hedge funds, real estate syndications, interval funds, structured notes—so you can translate the strategy into plain English, pressure-test the risks, and decide if it actually deserves a place in your portfolio.

The Executive’s Guide to Selling Company Stock Without Regret (Rules > Feelings)

Selling company stock is rarely a math problem. It’s an identity problem. You’re balancing loyalty, career risk, and a very human fear: sell and it rips higher… hold and it collapses. That’s why most executive stock plans fail in the moment—under pressure—without rules.

A “Rules > Feelings” policy fixes that. Start by defining what the stock is for (safety, freedom, goals, or long-term wealth). Then measure concentration with two numbers—% of net worth and % of liquid investable assets—so you’re not guessing. From there, pre-commit to simple rules: sell enough to cover taxes at vest, diversify on a schedule (not a mood), use thresholds to prevent one huge decision, and reinvest proceeds into your target allocation so selling feels like progress—not loss.

RSU Withholding Is Not Tax Planning: The Surprise Bill Playbook

Most executives learn this lesson the expensive way: RSU withholding is not your tax bill. It’s a default setting—usually a flat “supplemental wage” rate—that often has nothing to do with your real marginal bracket once salary, bonus, spouse income, and investment income stack together. The result is predictable: a great year on paper, and an uncomfortable check in April.

The fix isn’t complicated. Build a simple RSU system: map your vesting calendar, estimate your true marginal rate, compare it to what’s actually being withheld at each vest, then close the gap with either higher W‑2 withholding or estimated payments. Add one written rule you follow every time (no improvising), and you turn taxes from a surprise into a routine—while also keeping employer-stock concentration from quietly becoming your default portfolio.

The Busy Executive’s Annual Money Checklist (30 Minutes/Quarter)

If you’re a busy executive, you don’t need more financial content—you need a repeatable system. Most high earners aren’t “bad with money.” They’re busy. So money decisions get made in bursts: tax season, open enrollment, a market scare, a job change. That’s how you end up with an expensive, ad-hoc setup and a plan that only exists in your head.

Here’s the alternative: four 30-minute check-ins per year. Put them on your calendar and treat them like a board meeting for your balance sheet. In Q1 you set the baseline (one-page snapshot + quick tax projection). In Q2 you tighten the bolts (benefits, insurance, beneficiaries). In Q3 you manage concentration risk (equity comp and portfolio guardrails). In Q4 you execute the high-impact moves (withholding, charitable strategy, tax-loss harvesting, retirement contributions).

Not intense. Consistent. And designed for real life.

How to Build a Personal Investment Policy Statement You’ll Follow in a Drawdown

Most investors don’t blow up their plan because they lack intelligence. They blow it up because drawdowns compress time horizons, amplify loss aversion, and let headlines hijack decision-making. In calm markets, everyone is “long-term.” In a -20% market, even smart people start negotiating with themselves.

A personal Investment Policy Statement (IPS) is the antidote—not a 40-page institutional document, but a one-page set of rules you can follow when markets are loud and emotions are expensive. It clarifies what the money is for, your real definition of risk, your target allocation and rebalancing bands, and (most importantly) what you will do at -10%, -20%, and -30%—before you’re in it.

The goal isn’t to predict the bottom. It’s to prevent a permanent mistake.

The Anti-Budget: A Cash Flow System That Works When Income Is Lumpy

If your income is lumpy, traditional budgeting advice breaks fast. It assumes predictable paychecks and stable months—so you end up overspending in “good” months and stressing in “slow” ones. The problem usually isn’t discipline. It’s volatility.

The anti-budget is a simple cash flow system built for uneven income: define your Base Life number (non‑negotiable monthly costs), build a runway fund to smooth the gaps, and use a two-tier checking setup so your day-to-day account stays stable while a buffer absorbs the chaos. Then, when a big month hits (bonus, commission, distribution), you run a pre-written waterfall—taxes first, runway next, then investing, then guilt-free lifestyle.

Less tracking. More structure. And a system that keeps your financial life steady even when your income isn’t.